Building an Emergency Buffer

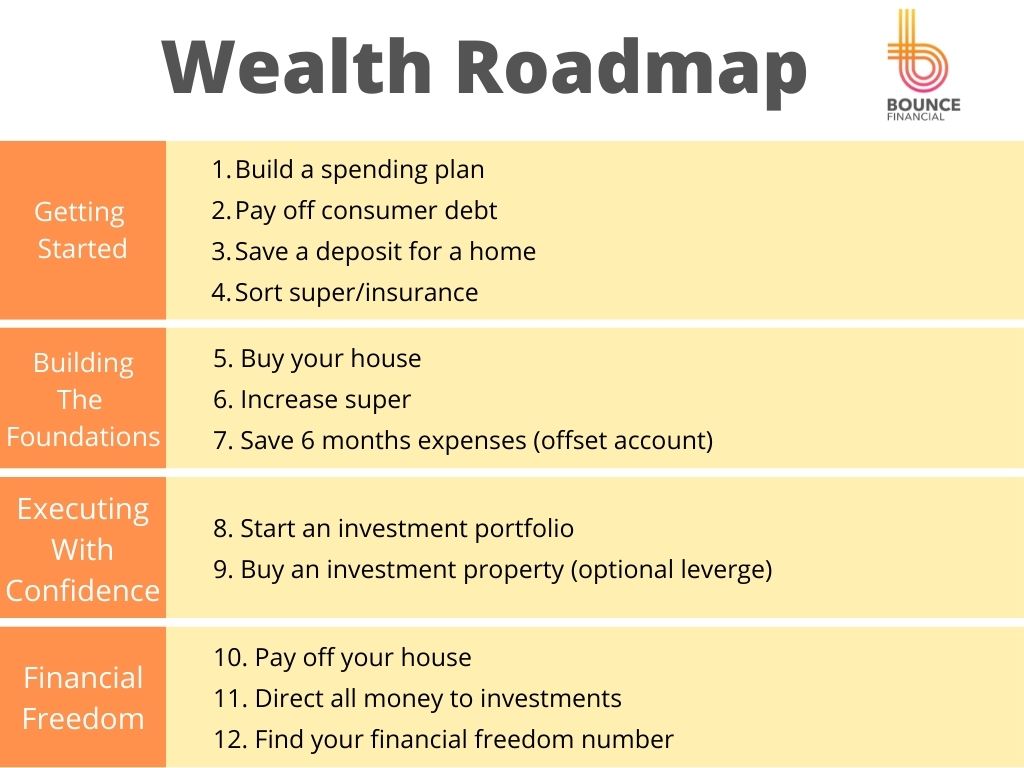

If you’ve been following Bounce Financial for a while, you may be aware of our Wealth Roadmap. This is the steps we recommend you go through to build wealth. If you haven’t already, check out our blog on the Wealth Roadmap.

Step 7- Save 6 months expenses

Step 7 of the Wealth Roadmap is to save 6 months of expenses in an offset account as an emergency buffer. For most of our clients who own their home but aren’t ready to invest yet, this is the step we do before commencing investment.

Why do I need an emergency buffer?

Human beings are interesting creatures. When we are asked to describe our past, we will usually describe some wins and some losses. When we are asked to picture our future however, we tend to only mention likely positive things.

Things can and do go wrong. In this instance, having a lot of cash aside can be a valuable exercise.

For this step, I recommend 6 months of expenses. Why 6 months? Well this is the amount of time I would be comfortable you can find another job if for any reason you quit or were fired from your job.

Depending on a number of factors including whether you have kids, how secure your job is etc, you may want more or less but at least 6 months before you start to invest makes a lot of sense.

Can’t I just use Credit Cards?

There is a comfort in knowing that your finances are rock solid. Knowing that you can tell your boss to go to hell at any point and be ok for 6 months without having to rack up a credit card and chase your tail for a year afterwards paying it back will provide you with a freedom that is unparalleled.

Should I invest my emergency fund?

The purpose of an emergency fund is to have immediate access to money whenever you want, regardless of market conditions. When it comes to investing, there may be bad times that you don’t want to access your investments.

These bad times in the market tend to correspond with bad times in employment so we really don’t want to invest your emergency fund.

Where should we put the emergency fund?

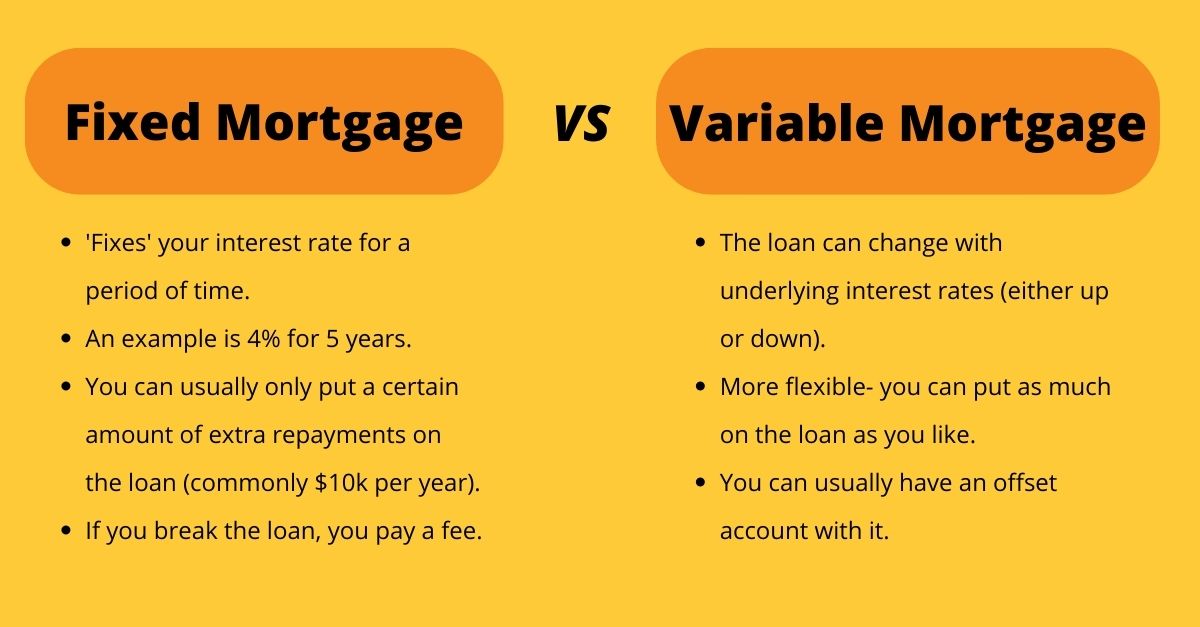

If you’ve completed step 5 and bought your house, the best place you can put this money is in an offset account.

An offset account is a normal bank account attached to your home loan that ‘offsets’ the interest.

The benefit of this is you are essentially receiving a return on this money similar to if you paid off your house. For example, if your home loan rate is 4%, you are receiving a 4% return.

The thing about offset accounts however is in 99% of cases, they only work with variable loans. So make sure you don’t fix the entirety of your loan and have enough in your variable account to allow you to add to the offset account enough that doesn’t exceed how much can be offset.

How should I save 6 months of expenses?

If you’ve completed step 1 and come up with a spending plan, you should have an idea of how much you can save. Your saving rate is the amount of money left over after you’ve spent all the money to live your life. This includes things that are coming up that you haven’t spent yet such as Christmas or holidays.

How much you save really depends on how much you are willing to forego now to have a better tomorrow. A good rule of thumb is to aim for at least 20% of your post tax income.

So if you and your partner earn $120k each ($88k after tax), you could be aiming to save $35k after tax.

This really depends on where you are at in your life (e.g. maternity leave will be more difficult). But coming up with a savings rate you are comfortable with and sticking to it will help you succeed.

What happens once I save 6 months of expenses?

This really depends on what your goals are. As a general rule, I try to suggest refraining from investing until you have a good savings buffer. You want to be certain that if investment markets turn against you or interest rates go up, that you have a rock-solid financial position.

You may choose to simply keep saving into your offset account with the goal of paying off your house. If you’re looking to upgrade, renovate or anticipate income dropping in the future, this may be a great use of your money.

Alternatively, you may want to look to start investing which are addressed in other blogs.

Should I ever have more than 6 months of expenses saved?

Saving 6 months of expenses is the minimum I suggest before you start investing. In reality, you should be focussing on always directing money towards paying off your house.

Once you’ve paid off your mortgage, having 6 months of money set aside and then focussing entirely on investing makes sense.

As always, you can do this in any way you want and each person’s goals will dictate how we go about this. If you would like to chat about your own plan and how we can set up these steps, then please reach out. We are always here to help.

About the author: Ben Brett

Ben Brett owns and operates Bounce Financial with his wife, Cara. Having started his career as a Corporate Lawyer, Ben has always had a passion for helping make the complex things simple. Follow Ben on LinkedIn at www.linkedin.com/in/ben-brett/