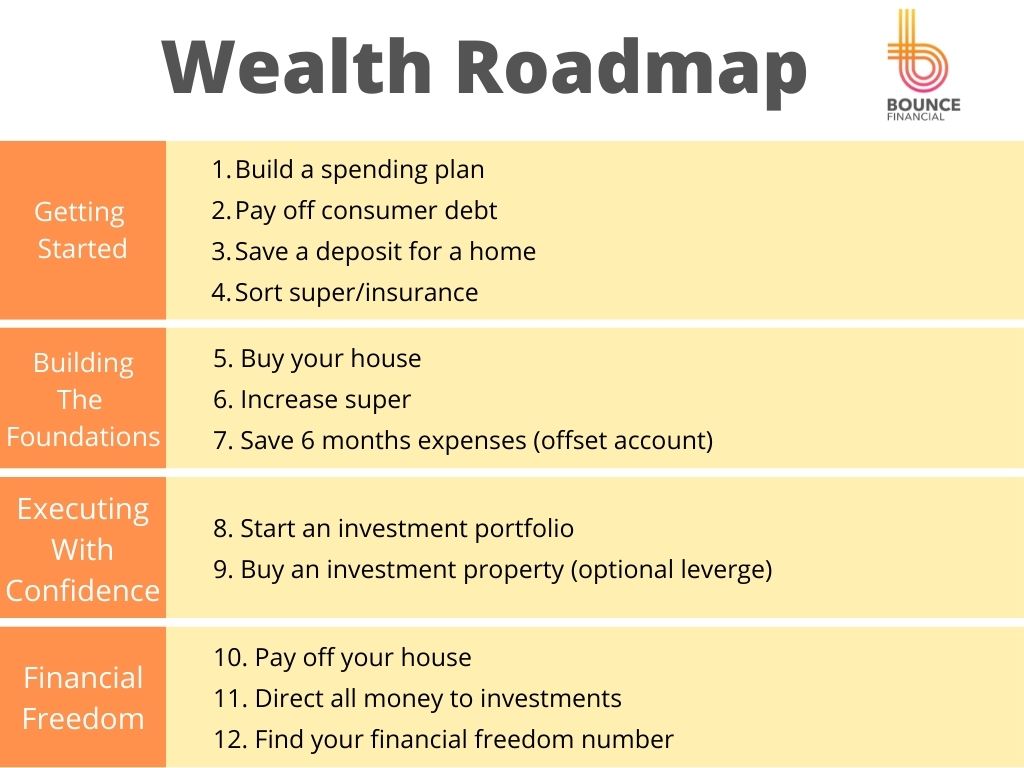

The Wealth Roadmap

If you want to build wealth, you need a (financial) plan. Whilst everyone’s plan should be different, through working with hundreds of families, we have formulated a Wealth Roadmap to provide you with a great starting point.

In future blogs, I’ll address some of these topics individually, but this is a high-level breakdown of these steps. So, let’s work through the roadmap.

GETTING STARTED

Considering the average age of my clients are 35-65, it’s rare that they are solely in the ‘Getting Started’ phase. As part of our advice however, we go back to this stage and work through these fundamental building blocks.

- Build a spending plan

The first step in this phase is building a spending plan. Even for high income earners, you need a plan on how you are going to spend your money so that you can send money to investments with certainty.

How much you choose to save is a personal decision, but a common rule of thumb is to try and save about 20% of your post-tax income. This means if you and your partner earn $100k each (before tax), you should be aiming to save about $30,000 a year. This is obviously a lot more difficult for lower earners and should be scaled down to reflect your situation (or scaled up for higher earners).

For my client’s, we work out how much their lifestyle costs to live and determine what is left. If they decide that isn’t enough savings, we strategically remove lifestyle expenses to find the right balance.

- Pay off consumer debt

The next step is to pay off all consumer debt. Too often I see people investing when they have credit cards or personal loan debts. The economics on this rarely make sense.

- Save a deposit for a house

The majority of my clients want to buy their own house and saving the deposit is the first big financial hurdle of your adult life. This is where having a solid spending plan will assist you.

- Sort super/insurance

Most people assume that their super fund has made decisions around their investment options and insurance which suit their needs. They haven’t and you should look to get this sorted ASAP.

BUILDING THE FOUNDATIONS

This stage is all about building up moats which will provide you with financial security before you start making decisions which come with more investment risk.

- Buy your house

This is a big step and one in which we work with our clients to determine how much they should spend based on not only their finances now, but their finances in the future should they start having children etc.

- Increase super

The contributions your employer makes to super are unlikely going to be enough for you to live the retirement you want. Starting the process of increasing your contributions, even a small amount, will make a big difference to your retirement.

- Save 6 months expenses (offset account)

This is a powerful step and one most people tend to skip. Before you start investing, you need a plan on how you are going to survive when times get tough (because they do). You may have a medical emergency, be unexpectedly made redundant or a global pandemic may happen.

Having at least 6 months of expenses or more (preferably in an offset account) will allow you to invest without fear of having to access your investment prematurely.

EXECUTING WITH CONFIDENCE

Whilst it might seem like a lot of steps have taken place before you start investing, going through these steps allows you to have confidence that you can weather any storms as you introduce investment risk into your plan.

- Start an investment portfolio

If you have aspirations of reducing or ceasing work prior to 60, you’re going to need to start investing outside of superannuation.

Whilst you may choose to simply focus on paying down your house instead, dedicating a part of your savings to an investment portfolio can be a way of trying to achieve better returns than paying down your home loan solely.

- Buy an investment property (optional leverage)

Another option for investing is to buy an investment property. Investment properties can introduce a little more risk (as you are borrowing money to invest) so you want to ensure you are in a strong cashflow position. This leverage however can help accelerate your wealth goals.

FINANCIAL FREEDOM

I regularly meet with clients who have paid off a fair bit of their home (or it entirely) and are on their way to financial freedom but they drop the ball. Now is the time to be putting all of your excess money towards investments to quickly grow your wealth.

- Pay off your house

To be financially free, you need to get out of all debt, and this includes your family home. Surprisingly, this can be a mental challenge for a lot of people who feel uneasy about not having a mortgage.

- Direct all money to investments

Once you’ve paid off your house, you’ll have a LOT more money to dedicate to savings. Depending on your circumstances and when you intend to access the money, this should be directed to either your superannuation, investment portfolio or investment property debt (or a combination of these).

- Find your financial freedom number

Once you’ve paid off your home and are directing money to your investments, it won’t be long until your investment earnings are able to fund your lifestyle. In this step, we will work out how much money you need invested to start making decisions about when and how much you choose to work.

SUMMARY

There are a lot to these steps and in future blogs I’ll explore each one in more detail. As always if you have any questions, please reach out, we are here to help.

About the author: Ben Brett

Ben Brett owns and operates Bounce Financial with his wife, Cara. Having started his career as a Corporate Lawyer, Ben has always had a passion for helping make the complex things simple. Follow Ben on LinkedIn at www.linkedin.com/in/ben-brett/