Should you change your investments if the market is going to crash?

I received an enquiry this week from a client about whether we should change his super investments. For context, the share market has taken quite a tumble in the last week or two and a lot of experts are saying we should expect more.

This question obviously comes up quite a lot as a financial planner and the answer is a complex one. In this blog post, I’ll try to address my thoughts on the topic but if you have any concerns or questions, it’s always worth having a chat with your financial planner.

Who says the market is going to crash?

The first thing to understand is who is saying that the market is going to crash. It’s important to remember that fear sells, so newspapers are incentivised to make things appear worse than they are. When you read a scary news article that says, ‘the market dropped $10 billion dollars in one day’, it’s probably important to do some of your own research to determine if this is real or not. Nine out of ten times, it’s a normal day in the market and the journalists were struggling to come up with a good article for that day.

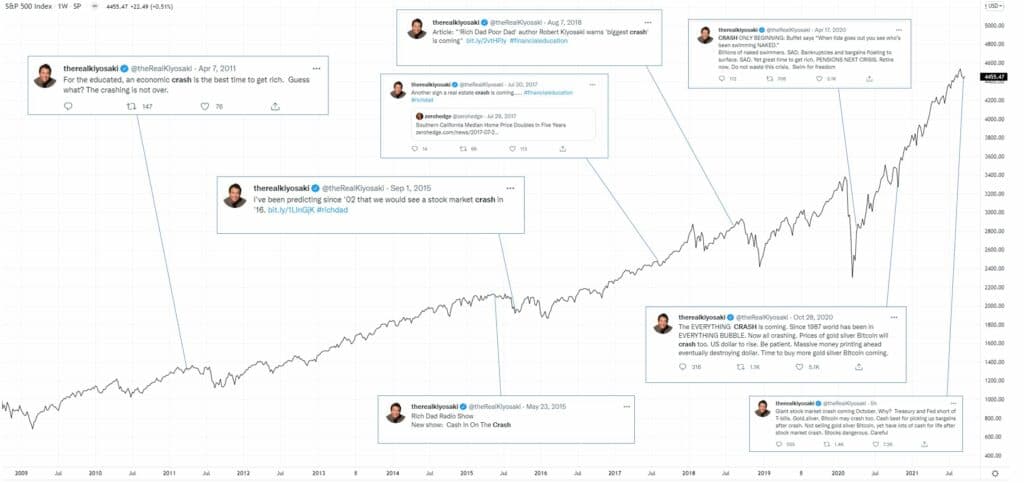

The other thing to be cautious of is so called ‘investment gurus’ who give dire predictions of market crashes. The one that comes to mind for me is Robert Kiyosaki, the author of “Rich Dad, Poor Dad” who has been particularly vocal lately.

These so-called experts predict market crashes every couple of months to remain relevant (usually so they can sell you something). In nearly all cases they are wrong but if you do this enough times, eventually you get it right.

In fact, Luc ten Have (@luctenhave) shared this great graphic of every time Kiyosaki has tweeted about a market correction and the subsequent market response. It really paints the picture:

But you know right? You can tell that the market is crashing?

You may agree with me that the experts don’t know what is going to happen but your gut tells you that you can tell the difference, am I right? This is normal. Everyone feels like they can tell when a market is going to top and when it’s going to bottom out. But you can’t.

It’s important to accept that for some investments, they go up and down in value and plan accordingly.

If I tried to time the market, what’s the worst that can happen? Surely I’ll get close enough!

If you decide to move all of your investments to cash right at the top of a market and move it all back to high growth stocks at the bottom, you will be financially better off. But this is a lot easier said than done.

I saw a lot of this during the market correction in 2020 in response to the Covid pandemic. A lot of people moved their investments to cash as markets dropped. What they didn’t foresee was the rapid recovery, all of which they missed as they remained in cash. I spoke with a lot of people who were still sitting in cash two years later waiting for the ‘market to drop back to where it was’.

Study after study has shown that on average, people who actively try to trade statistically perform worse than those who stay the course. You might be the exception, but why take that risk?

Don’t forget about distributions

There are more to investments than capital growth alone. If you are invested in property and shares, you usually receive rent or dividends. These are paid to you by way of distribution. If you sell off these investments, you are no longer entitled to the distributions.

Missing out on these can make a big difference to your investment performance over the long-term.

So should you change your investments?

In many cases, the answer is “no”. If you’ve got a good long-term plan, the best bet is to wait, continue to contribute (which is now occurring at a lower cost) and keep to your strategy. After all, it’s the money you invest now which is going to grow the most when markets return.

This however is a good time to reflect on your long-term strategy.

Has your reason for investing changed?

A fear of a market correction can be a sign that your investing strategy may not suit you anymore. The first thing to ask yourself is “has my reason for investing changed?”

A lot of the time when we are investing, we are doing so for a long-term plan. As this plan approaches however, your long-term horizon becomes a short-term horizon and you need to change your investments accordingly.

If your fear is based on the view that you intend to access your money in the next year or two, then perhaps now is the time to start considering changing your portfolio. It’s not uncommon for a market to take years to return to the same value so it’s important to always be aware of your goals when investing.

For my client I spoke to this week, we were discussing his superannuation. He is in his early 40s and not likely to have access to his super for another 20 years. Given his long-term time horizon, I suggested we stay the course and stay in a high growth investment.

He salary sacrifices to his superannuation which means that if the market does continue to go down, he will be continuing to invest at lower and lower prices. Once the market does return, these investments will be the ones to rise the most.

Summary

If I was going to summarise this blog, if you’ve got a long-term horizon and a solid investment plan, a market correction is not the time to be making changes. If however your investments don’t suit your goals, now might be the best time to take action.

This depends on how much the market has corrected and in some cases, it may be too late and you just need to wait it out. This is why I suggest reviewing your investment strategy (not just your investments) at least annually or when major changes to your plans occur.

As always, this is what we do, so if you’re looking for someone to help develop your strategy and assist you through it, please reach out.

About the author: Ben Brett

Ben Brett owns and operates Bounce Financial with his wife, Cara. Having started his career as a Corporate Lawyer, Ben has always had a passion for helping make the complex things simple. Follow Ben on LinkedIn at www.linkedin.com/in/ben-brett/