Investing for retirement- part one: understanding your investments

Like all investments, superannuation isn’t set and forget. What suits one part of your financial journey, may not suit the other.

In this article, I’ll break down how we go about recommending investment strategies for clients approaching retirement and why you should be focussed on this as soon as possible.

Why you should choose your investments in superannuation

There is a prevailing myth that once you’ve selected a super fund, you don’t need to do anything more. This couldn’t be further from the truth.

A super fund acts as the administrator of your superannuation balance. They ensure the account balance is accurate and the correct tax is paid. They also offer investment options which you can choose. If you decide not to choose which investment option you would like, they will have a default option.

Whilst the super fund is responsible for ensuring you pay the correct tax and your balance is correct, they aren’t obligated to make sure you have enough for retirement. Whilst they try their best, it’s important to understand that this is your responsibility.

If you fail to select your own investment, you run the risk that you will end up in an option which doesn’t suit you at all. Worse still, you may not realise this until you retire and are hundreds of thousands of dollars short.

How to pick the investments in your superannuation

Most people have the same ultimate goal from their superannuation, they want it to make as much money as possible. It therefore seems logical that the default option would be geared towards making a lot of money. But this isn’t the case.

As a general rule when it comes to investing, the amount of risk you take usually correlates to the return. When we refer to ‘risk’ in an investment sense, we refer to the risk that your balance may go down in value in the short-term (as opposed to the risk that you might lose it all).

When you are younger, it is generally appropriate to take more risk with your investments to achieve a greater return (within reason). This may mean that your super balance goes down in the short-term if markets crash, but overall, your return over the long-term should hopefully grow. This is why most young people are best placed in a high growth investment.

Where this starts to become an issue however is as you approach retirement.

Dealing with risk in retirement

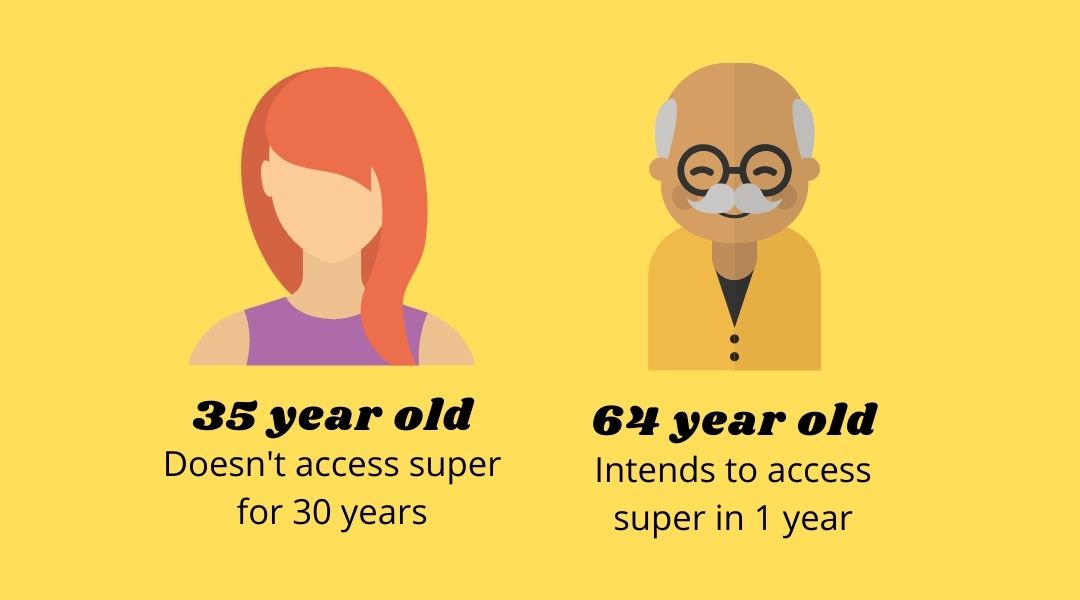

Let’s discuss an example comparing a 35 year old and a 64 year old approaching retirement.

Both the 35 year old and the 64 year old have their super balance in a high growth investment because they both want to earn as much money as possible for retirement.

Now let’s assume that the share market goes down in value 30% (this can and does happen).

For the 35 year old, this isn’t a big issue at all. They can continue to contribute to their superannuation and wait for the market to go back up.

For the 64 year old approaching retirement, this could be a disaster.

This is because the 64 year old doesn’t have years to wait for the market to recover. If they intended to retire at age 65, they will find themselves with a difficult choice. Do they retire and start pulling money out of their super at a loss? Or do they continue working?

If they do retire and pull money out, when the market does eventually recover, they won’t see the same gains that the 35 year old will enjoy. This puts them at risk of not having enough money for retirement.

This is why as you approach retirement, your investment strategy needs to change based on your intended draw-down from your super.

Default options- The lifecycle investments

Acknowledging that younger people are generally better suited to higher growth investments, and older people more conservative investments, a lot of the super funds have in recent years changed their default option to ‘lifecycle’ options.

These options change your investment strategy as you age to reduce the amount of risk (and subsequently the return).

Whilst this is definitely a step in the right direction, it really does add a whole new set of issues you should be concerned about.

CHANGING YOUR INVESTMENTS AS YOU AGE

In lifecycle investments, your investment strategy changes when you hit certain milestone birthdays. This happens regardless of what is occurring in financial markets which can cause major issues if you get unlucky with timing.

For example, let’s say that your investments are due to change when you turn 50 to sell off some of the higher growth investments. Now if markets are good, this may be a sensible strategy. But if markets are down, all you are doing is locking in that loss.

Once the investment markets go back up, you’ll never recover. Getting unlucky a couple of times could truly have a disastrous effect on your super balance.

DE-RISKING TOO EARLY

Everybody approaches retirement differently. For some people, on day one of their retirement (which can be as early as 60), they pull out all of their money. For others, they continue working for another 8 years and start drawing down small amounts to complement the Centrelink aged pension.

Your superannuation fund has no idea what you plan to do, so they play it safe.

Most of the products I see start de-risking you as early as your mid-50s. I reviewed a product for a client the other day that from 58 onwards, moved him to nearly 60% cash. Considering the average life expectancy in Australia is about 83, this client would have had over half of his super balance sitting in a low-interest bank account for up to 25 years.

Whilst I credit the super fund with doing the best they can, this really isn’t suitable for anybody.

So how should you invest for retirement?

Check out part 2 of this blog, where I address how we go about investing for our clients as they approach retirement.

About the author: Ben Brett

Ben Brett owns and operates Bounce Financial with his wife, Cara. Having started his career as a Corporate Lawyer, Ben has always had a passion for helping make the complex things simple. Follow Ben on LinkedIn at www.linkedin.com/in/ben-brett/